Why Accredited Investors Are Rethinking Fixed Income in 2026

For years, fixed income meant predictable returns through savings accounts, CDs, and bonds. However, in 2026, that definition is changing quickly.

Many investors are moving away from traditional options and into private credit and real estate-backed investments. The appeals are yield, structure, flexibility, and control.

As rates shift and markets remain uncertain, investors are looking for income strategies that offer consistency without long lockups or hidden fees. That is where private market Notes and fixed income alternatives like consumer credit investing are gaining traction.

The Problem With Traditional Fixed Income Investments

Traditional fixed income products still serve a role, but they come with clear limitations. CDs often lock up capital for fixed terms. Early withdrawals typically come with penalties that reduce returns. High-yield savings accounts can adjust rates at any time, often without notice.

For investors managing larger portfolios, these trade-offs create inefficiencies. Capital is either locked or underperforming. In many cases, it is both.

At the same time, inflation continues to pressure real returns. Even when nominal yields look competitive, purchasing power growth remains limited. This is why many investors are expanding beyond traditional investing options and turning toward private credit.

Why Private Markets Are Gaining Momentum

Private credit has emerged as a core allocation for modern portfolios. It offers something traditional fixed income often cannot: a combination of yield, structure, and asset backing.

Instead of lending through public markets, private credit involves directly funding loans, often backed by real assets like residential real estate.

This creates several advantages:

- Higher potential yields compared to traditional fixed income

- Returns driven by loan performance, not market sentiment

- More predictable income through structured payments

- Access to asset-backed investments

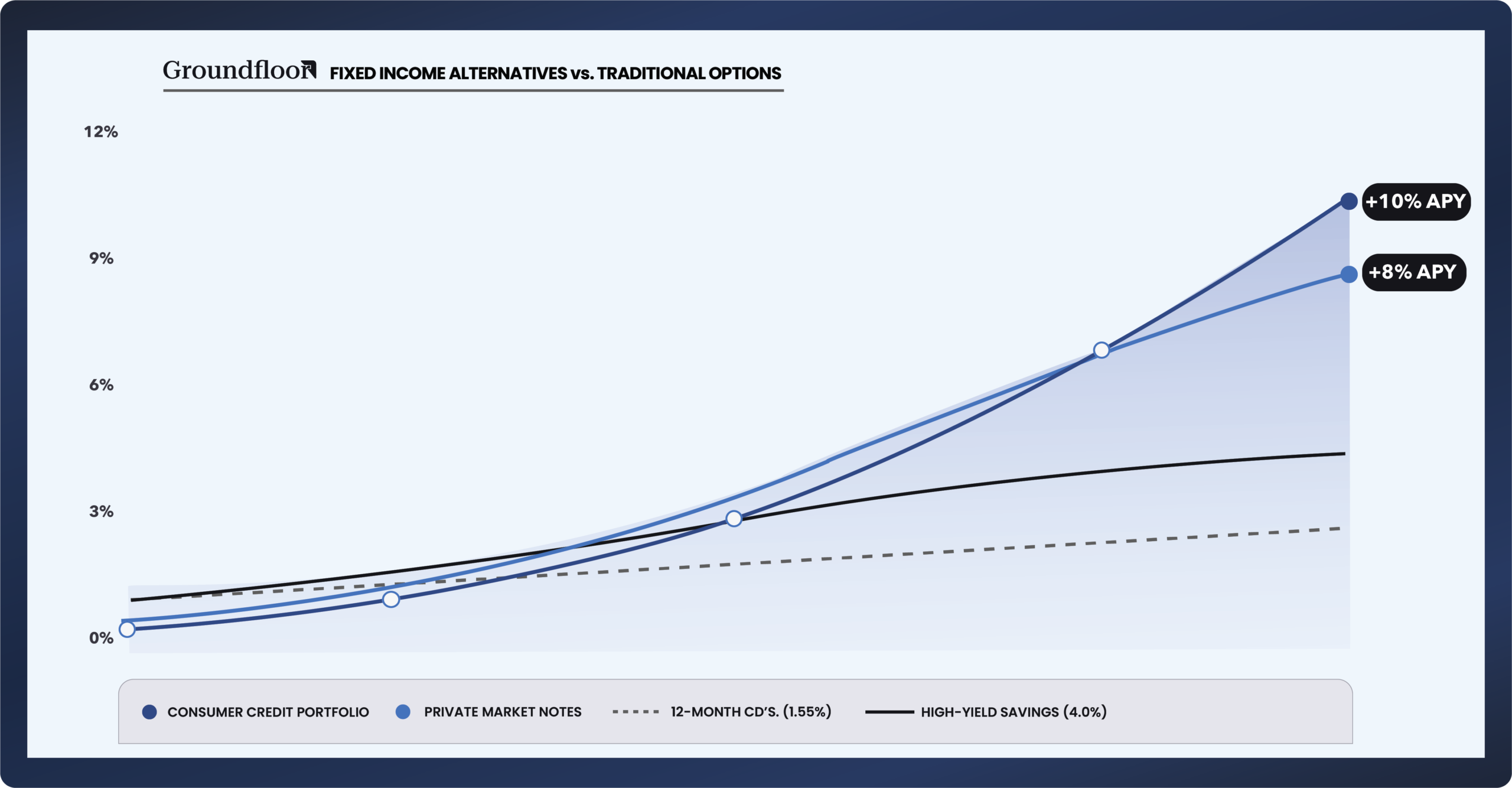

The Groundfloor 12-month Signature Note pays a fixed 8.25% annual rate, with monthly distributions, backed by first-lien position on every underlying real estate asset. The structure reads like a CD — fixed term, fixed rate, defined maturity — but the yield is more than four times the FDIC’s national average for a 12-month bank CD of 1.52%. Notes are SEC Reg A qualified, available to both accredited and non-accredited investors, and Groundfloor charges no management fees, no performance carry, and no investor fees.

Additionally, the Consumer Credit Portfolio II, is currently available for a limited window to accredited investors featuring a higher return of 10% fixed annual rate with quarterly distributions. The portfolio is backed by short term consumer micro loans. See a product review deep dive here.

Private credit and real estate investing options like Notes and the Consumer Credit Portfolio offer investors reliable, secure, fixed returns they can count on that are not affected by market fluctuations like traditional investments. The first Consumer Credit Portfolio offering sold out in just two weeks and is paying investors quarterly distributions at a fixed rate of 10% in full and on time.

What’s Driving More Investors to Alternatives?

Accredited investors are not new to alternatives. Many already have exposure to private equity, venture capital, or real estate syndications. However, their shift into private credit is driven by a different set of priorities.

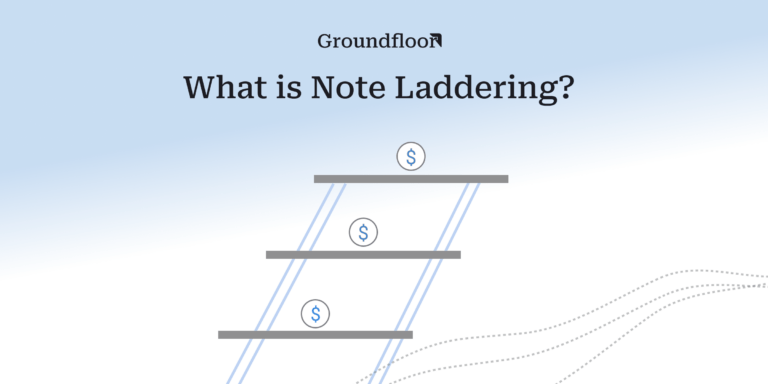

1. Liquidity Over Long Lockups

Traditional private market investments often require 7 to 10 year commitments. That limits flexibility and makes rebalancing difficult.

Private credit Notes, by contrast, typically operate on shorter timelines, ranging from one month to one year. This allows investors to redeploy capital more strategically.

Many accredited investors are now building a three-part private credit allocation using Groundfloor products: a core position in Consumer Credit Portfolio II for quarterly income, a Notes laddering strategy for monthly liquidity, and Preferred Notes to anchor the higher-yield portion of their income portfolio.

This blended approach creates staggered durations across 1-month, 3-month, 12-month, and 45-month investments, giving investors flexibility that traditional private equity structures often cannot provide.

2. Lower Fee Structures

Many private equity and fund-based investments charge both management fees and performance fees, which can significantly reduce net returns over time.

Private credit platforms like Groundfloor are structured differently. Returns are not eroded by layered fees, creating a more efficient income strategy. Groundfloor does not charge investor fees on Notes or Consumer Credit Portfolio investments, allowing investors to retain more of their returns.

3. First-Lien, Asset-Backed Security

Equity-heavy portfolios can experience volatility during market downturns. Private credit, especially first-lien debt, offers a different risk profile. Loans are backed by underlying assets or structured repayment streams, and investors are positioned ahead of equity holders in repayment. This creates a level of downside protection that many accredited investors are actively seeking.

The Consumer Credit Portfolio II expands this approach into consumer lending, offering diversified exposure to short-term loans that are actively underwritten and managed, with additional structural protections designed to support consistent performance.

4. Predictable Income

Instead of waiting years locked up for a liquidity event, private credit provides structured payments, often monthly or quarterly. For example, investors in the Signature Note are paid monthly with a current fixed annual rate of 8.25%, and Consumer Credit Portfolio investors are paid quarterly at a fixed annual rate of 10%.

For many accredited investors, the appeal is not just higher yield, but the ability to maintain liquidity while still earning institutional-style private market returns.

Blended yields across these products can exceed many public investment-grade fixed income allocations, while continuing to generate predictable monthly and quarterly cash distributions.

How Groundfloor Fits Into This Shift

Groundfloor provides access to private markets through real estate-backed Notes and consumer credit investment offerings, each with defined terms and fixed returns.

These investments are structured to offer:

- Short- to medium-term durations, ranging from 1 to 12 months for Notes

- Fixed rates with predictable monthly or quarterly income

- Exposure to real estate-backed loans and diversified consumer credit

- Transparent performance reporting

For accredited investors, this creates a complementary allocation alongside existing private market exposure. Rather than replacing private equity or venture capital, private credit can serve as a stabilizing layer within a portfolio, providing consistent income and helping balance overall risk.

What This Means for Income Portfolios in 2026

For income-focused investors, private markets are increasingly moving from the “alternative allocation” into the core fixed income portion of the portfolio.

As the Federal Reserve is expected to continue cutting interest rates into 2026, many investors anticipate yields on CDs, money market accounts, and Treasuries will continue compressing.

Private credit operates differently than traditional rate-sensitive fixed income because returns are tied more directly to loan performance, collateral quality, and borrower underwriting rather than short-term Fed policy.

This structural difference is one reason many investors view private credit as more resilient during periods when traditional savings and bond yields begin falling.

The Bigger Trend: From Yield Chasing to Portfolio Efficiency

Private credit delivers on these priorities in a way that traditional fixed income and many legacy alternative investments do not.

The Consumer Credit Portfolio II offers a 10% fixed annual rate with a minimum investment of $10K with a term of 45 months. It is only available for a limited window, until May 24th or fully subscribed. The first iteration was fully subscribed in two weeks.

Review the Consumer Credit Portfolio II

For non-accredited investors or those seeking a 12-month term, Groundfloor’s Signature Note is currently offering a fixed annual rate of 8.25% with monthly payments.

FAQ: Private Credit and Fixed Income Alternatives

Private credit refers to loans made by non-bank lenders directly to borrowers, rather than through public markets like bonds. These investments are often backed by real assets, such as real estate, and can provide fixed returns through structured interest payments. For investors, private credit offers an alternative to traditional fixed income with the potential for higher yields and more predictable income.

A fixed income alternative is an investment that provides predictable returns similar to bonds or CDs, but with a different structure. Private credit, real estate-backed Notes, and other asset-backed lending strategies are common examples.

They are seeking higher yields, shorter investment timelines, lower fees, and more control compared to traditional private market investments and fixed income products.

Private credit is generally less volatile than stocks because returns are based on loan performance rather than market pricing. However, it still carries risk, especially related to borrower repayment.

CDs are bank-issued and offer fixed rates but limited flexibility. The current national average for a 12-month bank CD is only 1.52%. Private credit investments are backed by real assets, often offer higher returns, and can include structured liquidity options depending on the product.

They are typically used as part of a fixed income or alternatives allocation, providing steady income and diversification alongside stocks and other investments. Groundfloor has a 100% repayment track record with Notes, with every investor receiving full principal and interest at term. Groundfloor investors have received 100% of expected principal and interest payments on Notes every month since 2018, reinforcing the platform’s emphasis on consistency and predictable income. Looking for a more flexible way to earn fixed returns? Explore Groundfloor’s real estate-backed Notes and see how private credit can fit into your portfolio strategy.