Why Investors Are Looking Beyond Traditional Fixed Income

Interest rates are less predictable, yields fluctuate, and traditional fixed income options often struggle to keep pace with inflation. At the same time, more investors are exploring private credit investing as a way to generate consistent income while diversifying beyond public markets.

Consumer credit is one of the fastest-growing segments within private credit. Historically limited to institutions, it is now becoming accessible to individual investors seeking stable, income-generating alternatives.

What Is Consumer Credit Investing?

Consumer credit investing involves funding short-term loans made to individuals for essential expenses. These loans are typically used for:

- Vehicle repairs

- Home emergencies

- Medical expenses

Unlike equity investments, which depend on asset appreciation, consumer credit investments generate returns through interest payments on loans. This creates a more predictable income stream.

The Groundfloor Consumer Credit Portfolio II provides access to this strategy through a diversified portfolio of short-term consumer loans, offering:

- 10.00% fixed annual returns

- Quarterly distributions

- A 45-month term with structured capital deployment

This structure allows investors to participate in an asset class that has traditionally required minimums of $250,000 or more, now available starting at $10,000 .

How This Private Credit Strategy Works

At a high level, the model is straightforward:

- Investors allocate capital into the portfolio

- Capital is deployed through Hive Financial Assets, a private credit manager

- Hive funds diversified consumer loans across multiple lenders

- Borrowers repay loans with interest

- Investors receive quarterly income distributions

Information provided by Hive Financial Assets, 2026

Hive processes tens of thousands of loan applications daily using AI-driven underwriting and focuses on short-duration loans, typically around nine months. This high-volume, short-term lending approach helps maintain consistent capital rotation and income generation.

Built for Predictable Income and Risk Management

One of the key advantages of consumer credit investing is its structural approach to risk. The portfolio includes multiple layers of protection:

- Lender and manager equity absorbs initial losses

- A diversified pool of loans reduces single-loan exposure

- Underwriting targets strong unit economics, with a 27% net margin after losses and expenses

This design helps prioritize income consistency and downside protection, which is central to fixed income investing.

Why Consumer Credit Can Perform in Volatile Markets

Consumer credit has historically shown countercyclical characteristics.

When economic conditions tighten, demand for short-term loans often increases as individuals seek liquidity for essential expenses. This can create a unique dynamic:

- Rising demand supports loan volume

- Short durations allow frequent repricing of risk

- Returns remain less correlated to stock market movements

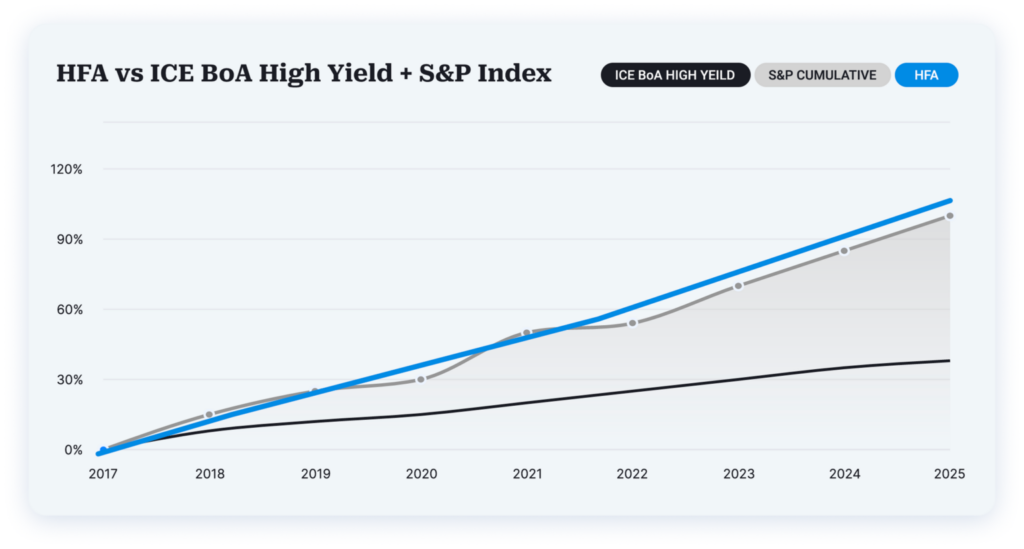

According to the performance data shown in the portfolio materials, Hive’s strategy has delivered positive returns even during months when the S&P 500 declined, averaging +1.21% during those periods. This makes consumer credit a potential stabilizer within a broader portfolio.

A Fixed Income Alternative for Modern Portfolios

Many investors today are rethinking how they build income-generating allocations. Instead of relying solely on traditional bonds or savings products, portfolios are increasingly incorporating:

- Private credit for consistent yield

- Real estate-backed debt for asset exposure

- Short- to medium-duration instruments for flexibility

Consumer credit fits within this shift as a private market fixed income alternative, offering:

- Defined returns

- Regular income distributions

- Lower correlation to public markets

For accredited investors, it can serve as part of a broader alternatives allocation designed to improve diversification and income stability.

Key Details: Consumer Credit Portfolio II

The current offering is structured as a limited, capacity-constrained investment:

- Target return: 10.00% annually

- Term: 45 months (36-month core plus 9-month rolloff)

- Distributions: Quarterly

- Minimum investment: $10,000

- Total offering size: $3,000,000

- Fees: None

- Tax reporting: 1099-INT

The first Consumer Credit Portfolio offering reached capacity in just two weeks and is currently distributing payments to investors in full and on time. We have expanded the cap and lowered the minimum for this offering to open access to more investors.

Limited Access and Timing

The subscription window runs from May 4 to May 24, or until fully subscribed, and allocations are filled on a first-come, first-served basis. Because the total offering size is capped at $3 million, access may close quickly once demand is met. Investors are encouraged to review the offering and transfer funds promptly.

Who This Type of Investment Is Designed For

This type of private credit investment is best suited for:

- Investors seeking fixed income alternatives

- Investors looking to diversify beyond stocks and bonds

- Individuals building a dedicated alternatives allocation

- Those interested in passive income with short and defined timelines

For many investors, this represents a way to access institutional-style strategies without traditional barriers like high minimums or long lockups.

How It Fits Within Groundfloor’s Platform

Groundfloor focuses on making private market investing more accessible, particularly in:

- Real estate-backed lending

- Fixed income alternatives

- Private credit strategies

Rather than operating as an open marketplace, Groundfloor offers a curated investing platform where opportunities are carefully structured, vetted, and selected to provide investors with access to private markets with greater transparency and alignment. Accredited investors also receive support from a dedicated client relationship manager to help evaluate opportunities and discuss portfolio fit.

See the alts.co review of the Consumer Credit Portfolio II here

Expanding Access to Private Credit

Private credit is no longer limited to institutions or reserved for those with $250K minimum to invest. As access expands, investors have more opportunities to build portfolios that generate income, diversify risk, and incorporate alternative asset classes.

Consumer credit investing is one of the newer ways to do this, combining:

- Short-term loan exposure

- Structured income distributions

- Institutional-grade underwriting

For accredited investors, the Consumer Credit Portfolio II offers a clear example of how private credit can be integrated into a modern portfolio.

If you are exploring fixed income alternatives or looking to diversify into private credit, you can also start with shorter-term options on Groundfloor. Groundfloor Notes offer flexible terms, consistent returns, and a simple way to begin building a private market allocation.

FAQs about Consumer Credit Investing

The portfolio includes multiple layers of protection, including lender and manager equity that absorbs initial losses before impacting investor capital.

Consumer loan demand has historically increased during economic stress, which may support continued loan origination and portfolio performance.

Loans typically fund essential expenses such as vehicle repairs, home emergencies, and medical costs.

Distributions are paid quarterly and deposited into your Groundfloor account. Quarterly distributions are currently being paid on time and in full to investors in our first Consumer Credit Portfolio offering.

The minimum investment is $10,000, significantly lower than traditional private credit funds requiring upwards of $250K for an investment of this kind.

There are no investor fees associated with this offering.