Designed for Simplicity

Groundfloor Notes are fixed-rate, fixed-term debt securities backed by diversified pools of short-term residential real estate loans originated and underwritten by Groundfloor. Every loan in the pool is secured by a first-lien position on the underlying property, and your yield is locked the moment you invest. Choose the term that fits your goals. No fees. Issued under SEC Regulation A and open to accredited and non-accredited investors.

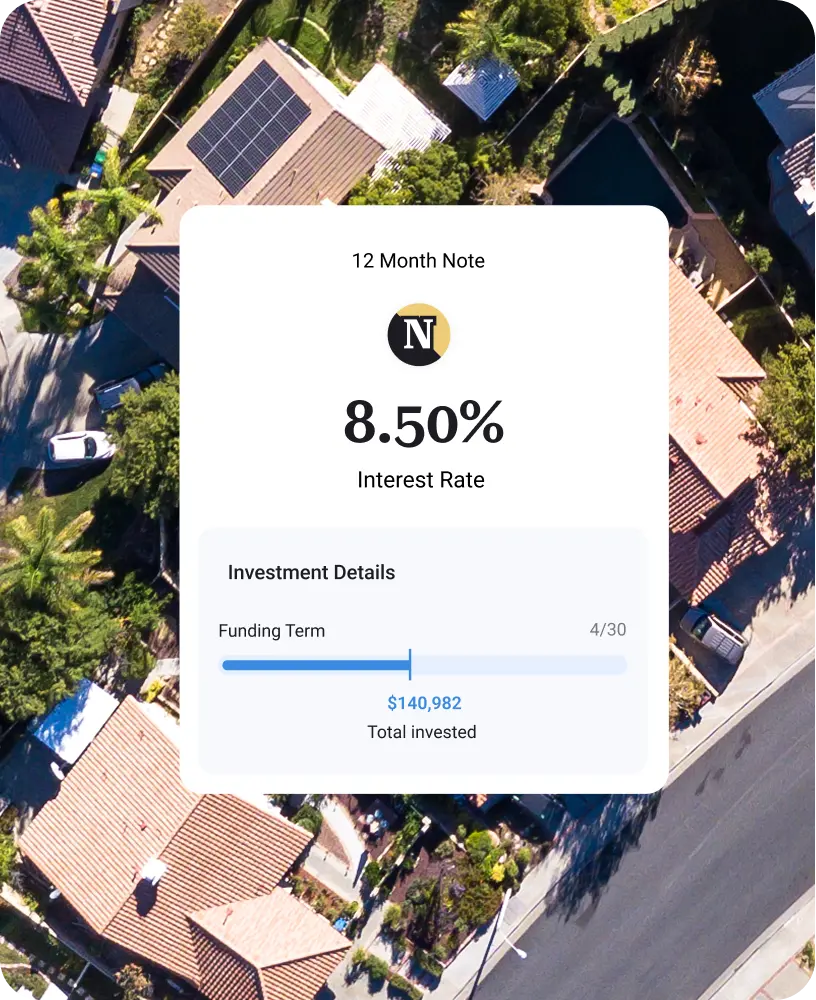

12-Month Note

FIXED APR

3-Month Note

FIXED APR

1-Month Note

FIXED APR

A two-year note paying 11.5% fixed interest, distributed monthly — 1.23x your capital through interest alone if held to maturity. Convert as early as 6 months. At the end of the term, choose your exit: convert into Groundfloor equity with discounted and bonus shares, roll into a future offering, or withdraw. Offered since 2017, with every investor repaid in full and on time.

Accredited investors only. Convertible Notes are obligations of Groundfloor and are not backed by a pool of real estate loans. Groundfloor has repaid all Convertible Note investors in full and on time since 2017. Investing involves risk, including possible loss of principal.

Limited time – Terms apply

The Notes program has paid out over $36.5 million in interest distributed and is reported in our SEC filings, alongside the 100% principal and interest payment record since 2018.

LOCK IT IN

Start with $1,000 in the 12-Month Signature Note. First-lien backed. Zero investor fees. New investors receive $100 bonus when using code NOTES100.

Pick Your Term

Groundfloor has originated $2.2 billion in real estate loans to vetted residential builders since 2013. Notes give you direct exposure to that loan engine without picking properties, managing tenants, or competing for deals

$100 minimum for 1mo/3mo, $1,000 for the 12mo Signature.

Short-term loans go to residential builders for renovations, rehabs, and new construction.

In any recovery, Groundfloor's first-lien claim is paid before junior debt or equity.

Monthly on the Signature Note, and at maturity on 1mo and 3mo Notes.

Monthly on the Signature Note, and at maturity on 1mo and 3mo Notes.

Structural Details

Every Note is backed by a first-lien position on every property.

When a residential builder takes a loan from Groundfloor, the loan is secured by a first-lien position on the property. In any recovery scenario such as a sale, refinancing, or foreclosure — the first lien holder is paid before any other claim.

That's the same structure a bank uses when it issues a mortgage. The difference: with a Groundfloor Note, you're the one earning the yield on the loan instead of the bank.

First-lien protection doesn't eliminate risk. It defines where you sit in line if something goes wrong. The position itself is the structural advantage.

First-lien holder

(you, via Groundfloor) PAID FIRST

Second-lien / mezzanine debt

PAID AFTER

Junior Debt

PAID AFTER

Equity (the builder)

PAID LAST

Capital stack in a typical residential real estate loan

First-lien holder (you, via Groundfloor) PAID FIRST

Second-lien / Mezzanine Debt PAID AFTER

Junior Debt PAID AFTER

Equity (the builder) PAID LAST

Capital stack in a typical residential real estate loan

100% Repayment Track Record

Every Note Groundfloor has issued since the program launched in 2018 has paid 100% of principal and interest. The track record lives in our SEC filings.

Through inflation, rate hikes, and a regional banking crisis — every Note has paid in full and on time.

Funded across 12 years of operating history

Individual investors on the platform

HOW NOTES COMPARE

Short-duration fixed income products differ in structure as much as in yield. Here is how the 12-month Signature Note sits next to the alternatives investors typically consider.

$15,000 INVESTED · 12 MONTHS

JUly 2026 RATES

JUly 2026 RATES

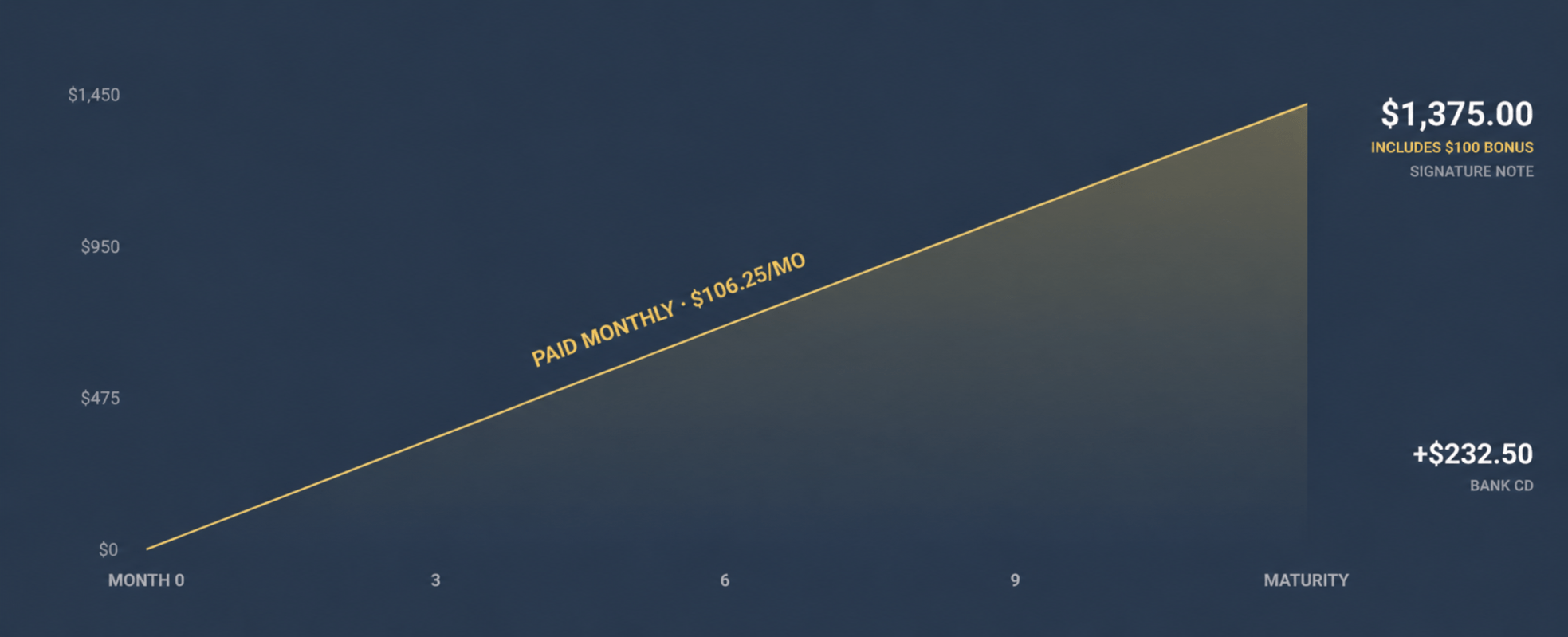

$15,000 in a Groundfloor 12-Month Signature Note earns $1,375 in interest + starting bonus over 12 months at 8.5% fixed rate.

You’ll receive $106.25 in interest each month, plus the $100 starting bonus.

The same $15,000 in a 12-month bank CD at the FDIC national average of 1.55% earns $232.50, paid once at maturity.

That’s $1,142.50 more in total earnings over the same 12-month period.

+$1,142.50

More interest than a CD over 12 months

Signature Note vs. 12-month bank CD on a $15,000 investment

New investors: invest $1,000+ in Notes and get a $100 bonus on top of your interest with NOTES100 — on a $15,000 Signature Note, that lifts first-year earnings to $1,375.00.

1.55% APY · FDIC national average · Paid at maturity

$100 minimum for 1mo/3mo, $1,000 for the 12mo Signature. Reg A qualified.

Illustrative comparison. Assumes $15,000 invested at 8.5% fixed APR in the Groundfloor 12-Month Signature Note (monthly distributions of $106.25 × 12 = $1,275.00 total interest) versus a 12-month bank CD at the June 2026 FDIC national average yield of 1.55%. Notes are not bank deposits and are not FDIC-insured. Past performance does not guarantee future results. $100 new-investor bonus available for a limited time on first investments of $1,000+ in Notes, subject to promotional terms. Bonus is not interest and not included in the chart figures.

| GROUNDFLOOR SIGNATURE NOTE |

12-MONTH BANK CD (FDIC AVG) |

OPEN-ENDED RE INCOME REIT |

HIGH-YIELD SAVINGS |

|

|---|---|---|---|---|

| Stated yield | 8.50% fixed APR | 1.55% APR | ~8% variable | ~3.5–4% variable |

| Rate locked? | Yes — locked at investment | Yes — locked at investment | No — adjusts monthly | No — bank can change |

| Term | 12 months, defined | 12 months, defined | Perpetual / open-ended | None |

| Distributions | Monthly | At maturity | Monthly | Monthly accrual |

| Collateral / backing | First-lien on real estate | FDIC to $250K | Equity claim on portfolio | FDIC to $250K |

| Investor fees | Zero | None | ~1% AUM annually | None |

| Minimum | $1,000 | $100+ | ~$100 | $0–$1,000 |

| Accreditation | No — open to all | No | No — open to all | No |

| Track record | 100% paid since 2018 | FDIC backing | ~4 years operating | FDIC backing |

LOCK IT IN

Lock in your rate for the entire term the moment you invest.

WHO NOTES ARE FOR

Notes are flexible, high-yield investments designed for any investor.

The Signature Note delivers fixed 8.5% for the same 12-month commitment — first-lien backing instead of FDIC backing. Different protection, materially different yield.

Notes give you a fixed alternative with monthly flexibility — high yields without giving up control of your cash for long lockups.

QUESTIONS

Notes are designed to be understood. If your question isn’t here, our Investor Success team is available at [email protected] — we don’t outsource to a chatbot.

A Note is a fixed-rate, fixed-term debt security — predictable income for a defined period.

We also offer an actively managed REIT with a 3-year vintage targeting a 9–10% IRR, individual LROs, and curated limited availability private market offerings for accredited investors. Many investors hold multiple.

LOCK IT IN

The Signature Note is our most popular investment. Start with $1,000, receive your $100 bonus with NOTES100, and add more capital over time.