For years, fixed income investments like CDs, savings accounts, and bonds were considered the “safe” part of a portfolio. They offered stability, predictable returns, and a place to park cash. But in 2026, many investors are questioning whether traditional fixed income is still doing its job.

Why Traditional Fixed Income Is Falling Short

High-yield savings accounts and CDs are losing momentum. As of May 2026, the average 1-year CD is hovering around 1.9% APY, while inflation is expected to rise to about 3.4% over the next year and remain near 3% over the next 5 years.

Many traditional fixed income options, where investors typically park their cash, are no longer keeping up with inflation or only barely doing so. Over time, that can meaningfully limit long-term wealth building.

At the same time, interest rates are becoming less predictable. Changes from the Federal Reserve ripple through fixed income products quickly, and those adjustments often happen silently in the background of investor accounts. A high-yield savings account offering 5% APY today may drop to 3% before you even think to check.

This is exactly why more investors are starting to explore fixed income alternatives that aim to deliver more consistent, inflation-beating returns that don’t rely on federal rates and market swings.

What Investors Are Doing Instead

Because of the prominence of less-attractive yields, more every-day investors are exploring fixed income alternatives. These are investments designed to generate consistent income with higher potential returns than traditional options.

Some of the most common fixed income alternatives include:

- Consumer Credit

- Real estate-backed investments

- Asset-backed lending strategies

Historically, many of these opportunities were limited to institutional or accredited investors. However, that is changing. New regulatory frameworks are making private market investments more accessible to individual investors.

As a result, investors now have more ways to earn income and diversify their portfolios outside of traditional banks and bond markets.

Rethinking the Role of Fixed Income in a Portfolio

Fixed income still plays an important role in a diversified portfolio. However, how investors approach it is evolving.

Instead of relying entirely on traditional products, some investors are shifting toward a more balanced structure. One emerging approach is a 50/30/20 allocation:

- 50% in core holdings like index funds and traditional assets

- 30% in growth-oriented investments

- 20% in alternatives, including private credit and real estate-backed income

This alternatives portion is designed to provide steady income while reducing reliance on public markets.

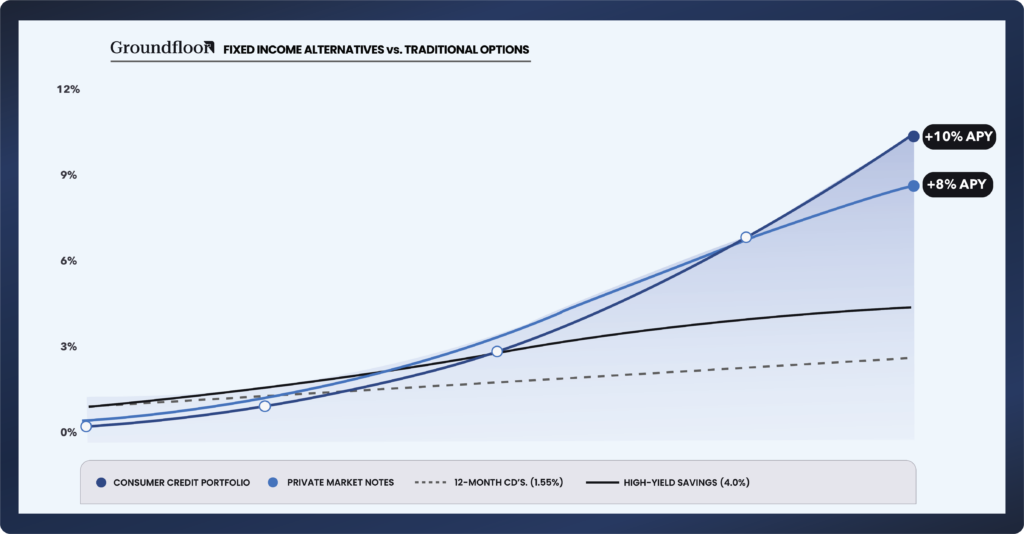

Comparing Fixed Income Alternatives to Traditional Options

When comparing fixed income alternatives to CDs or savings accounts, the key difference is return potential.

Traditional products:

- Typically offer 1% to 4% yields

- Are not highly liquid

- Are sensitive to changing interest rates

Fixed income alternatives:

- May offer returns in the +8% range (sometimes higher for accredited investors, like the 10% fixed annual rate Consumer Credit Portfolio II)

- Are often backed by real assets or credit structures

- Provide more consistent income over defined terms

- Do not rely heavily on federal rates, market swings, or world events

Of course, these fixed income investments come with different risk profiles and liquidity considerations. However, for many investors, the potential for higher income and less volatility is worth exploring as part of a diversified strategy.

A New Way to Generate Income

One example of a fixed income alternative is real estate-backed Notes. These investments allow individuals to earn fixed returns over short durations, ranging from one month to a year.

Instead of relying on bank interest rates, returns are generated from underlying real estate loans. Interest earned is pooled and distributed on a fixed-rate, fixed-term basis to investors. This structure provides reliable, predictable income while being less directly tied to fluctuations in federal rates. For investors looking to move beyond traditional fixed income, these types of investments offer a way to target higher yields while maintaining a focus on passive income.

Consumer Credit Investing

In addition to private market notes, Groundfloor just opened access to the Consumer Credit Portfolio II, the second iteration of a private credit investment opportunity for accredited investors. Offering a 10% fixed annual return paid quarterly, the portfolio is backed by small consumer loans for things like vehicle repairs, home emergencies, and medical expenses.

The first Consumer Credit Portfolio sold out in just two weeks, and is paying quarterly distributions on time and in full. The window to invest is limited, open through May 24th or until fully subscribed.

See more on the Consumer Credit Portfolio II

The Bottom Line

Fixed income is not going away, but it is changing. Investors are becoming increasingly unhappy with low rates and long lockups.

With inflation reducing real returns and rates shifting over time, many investors are looking beyond CDs and savings accounts. Fixed income alternatives, including consumer credit and real estate-backed investments, are becoming a larger part of modern portfolios.

For those seeking higher income potential, exploring these options may be the next step in building a more balanced investment strategy.

FAQs About Fixed Income Alternatives

Fixed income alternatives are investment options designed to generate steady income with higher returns than traditional savings accounts or bonds.

They carry different risks than traditional products but can be relatively stable when backed by real assets and diversified.

Many options offer returns above 8%, depending on the investment type and risk level. Accredited investors often have access to higher-yield opportunities.

Most investments have set terms, so they’re potentially less liquid than savings accounts but often shorter than traditional bonds. The shortest-term investment with Groundfloor is the 1-month Note.

Alternatives have traditionally been reserved for institutions and high net worth accredited investors, but access is expanding. Many platforms, like Groundfloor, now allow everyday investors to participate at accessible minimums with the same high yields.

They typically offer much higher returns (over 4x), much more liquid terms, and are less affected by interest rate changes. The national average rate for a 12-month CD in 2026 is currently 1.9%, while Groundfloor’s 12-month Note sits at 8.25%.