If you’ve built up your savings, you’ve probably faced an important question: how can you put that money to work without giving up access to it for years?

High-yield savings accounts offer liquidity, but rates can change at any time. Certificates of Deposit (CDs) provide fixed returns, but typically offer lower yields and often charge penalties for early withdrawals. Many investors are looking for an approach that provides higher fixed income while still creating regular opportunities to access their capital.

That’s where note laddering, also called note stacking, comes in.

Over the years, we’ve seen many Groundfloor investors use this strategy to create a more predictable stream of income while maintaining recurring opportunities to reinvest or withdraw capital. Whether you’re building a fixed-income allocation or looking for an alternative to CDs and savings accounts, note laddering is a straightforward strategy worth understanding.

What Is Note Laddering?

Note laddering is the practice of spreading your investment across multiple Notes with staggered maturity dates. Groundfloor Notes are fixed-income investments backed by diversified pools of real estate loans, offering defined terms and fixed rates of return. Since Notes launched in 2018, Groundfloor has paid 100% of principal and interest owed to Note investors on time.

Instead of investing all your money into a single Note, you divide your capital across multiple Notes that mature at different times. As each Note reaches maturity, your principal and earned interest are returned, giving you the flexibility to withdraw the funds, use the income, or reinvest into a new Note.

The strategy balances higher fixed-income potential with recurring access to capital. Rather than waiting for one large investment to mature, investors create a schedule of recurring maturity dates that provide ongoing opportunities to generate cash flow, reinvest, or adjust their allocation as financial goals change.

The goal is simple: create recurring access to your capital while continuing to earn fixed returns that may exceed those offered by many traditional savings products.

How Note Stacking Works

Let’s assume you have $15,000 in savings available to invest.

Rather than investing the entire amount into one Note, you could build a simple ladder using three separate 3-Month Notes.

Example of a $15,000 Note Ladder

January 1st

- Invest $5,000 in a 3-Month Note earning 6.00%

February 1st

- Invest $5,000 in a 3-Month Note earning 6.00%

March 1st

- Invest $5,000 in a 3-Month Note earning 6.00%

Once the ladder is established:

April 1st

- January Note matures. Receive your principal plus earned interest and choose whether to withdraw or leave it alone to automatically reinvest.

May 1st

- February Note matures. If you reinvested the last note and need liquid cash now, you can withdraw. Or, let it automatically reinvest to keep working.

June 1st

- March Note matures. Withdraw or reinvest.

From that point forward, capital becomes available every month. You can withdraw funds as Notes mature or continue reinvesting to maintain your ladder.

This structure creates a rhythm of recurring maturity dates that many investors find useful for managing cash flow. Instead of having all $15,000 tied to one single maturity date, a note ladder provides regular opportunities to access part of your capital while the remainder continues earning interest.

If you maintained this $15,000 ladder for a full year and continuously reinvested each maturing 3-Month Note, you would earn approximately $900 in interest at a 6.00% annual rate.

By comparison, the same $15,000 invested in a traditional CD earning the current national average rate of 1.65% APY would generate approximately $247.50 in interest over the same period, and would lack the monthly access to your capital.

That’s approximately $652.50 more annual income than the average CD while still creating recurring opportunities to access your capital throughout the year.

Building a Hybrid Note Ladder

Some investors prefer a combination of shorter-term liquidity and longer-term fixed returns.

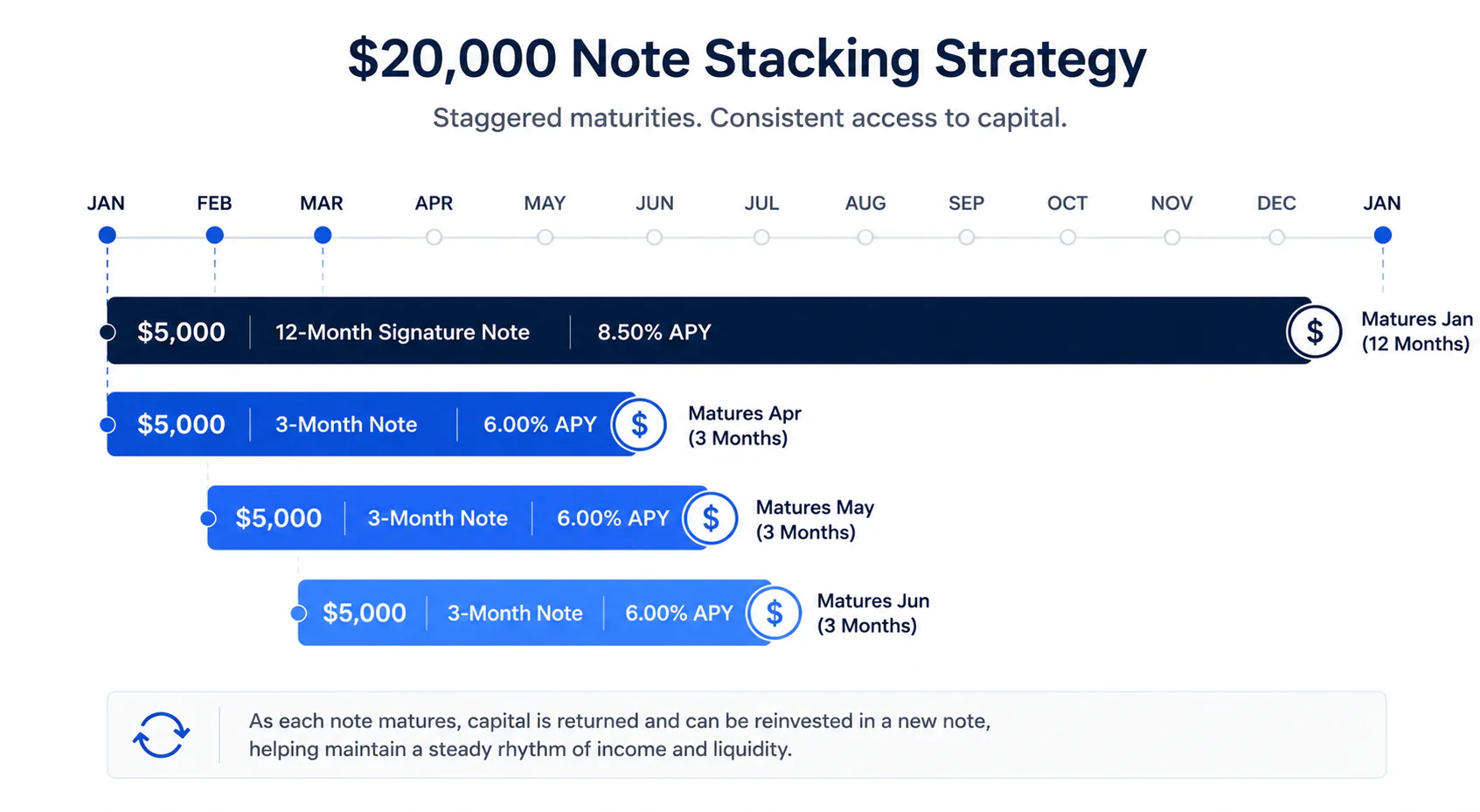

For example, a $20,000 note stacking strategy could look like this:

- $5,000 in a 12-Month Signature Note earning 8.50%

- $5,000 in a January 3-Month Note earning 6.00%

- $5,000 in a February 3-Month Note earning 6.00%

- $5,000 in a March 3-Month Note earning 6.00%

In this example, the 12-Month Signature Note serves as a longer-term income-producing investment paying interest monthly while the staggered 3-Month Notes provide recurring opportunities to access capital.

Beginning in April, one Note matures each month. Meanwhile, the 12-Month Signature Note continues earning its fixed return and paying interest monthly until maturity.

Investors who want even greater liquidity often use the 1-Month Note, currently earning 5.00%, to keep a designated portion of their portfolio available for monthly withdrawals or reinvestment.

Why Investors Use Note Laddering

Every investor’s goals are different, but note laddering is commonly used for several reasons.

Create Consistent Cash Flow

One of the biggest advantages of a laddered strategy is creating recurring maturity events. Instead of waiting for a single maturity date, portions of your investment become available throughout the year, supporting reinvestment, planned spending, or portfolio rebalancing. Many investors start with the 1-month Note and at maturity, invest a partial amount into a 3- or 12-month Note for higher returns while still maintaining monthly liquidity.

Maintain Access to Capital

Traditional CDs often impose penalties for early withdrawals. With a note ladder, investors know exactly when portions of their capital will become available because each Note has a defined maturity date.

Reduce Reinvestment Risk

Interest rates change over time. By staggering investments, you avoid committing your entire investment portfolio at one point in time. As Notes mature, you can evaluate current rates before deciding whether to reinvest.

Build a Fixed-Income Allocation

Rather than relying exclusively on savings accounts, CDs, or bond funds, a note ladder provides another way to generate fixed income while maintaining defined maturity dates and recurring access to capital.

For investors looking beyond traditional savings products, note laddering offers a different approach to generating income while maintaining recurring access to capital.

Who Should Consider Note Laddering?

Note laddering may be worth considering if you:

- Have savings earning less than today’s Note rates.

- Want an alternative to high-yield savings accounts or CDs.

- Prefer fixed returns over stock market volatility.

- Are building a passive income strategy.

- Want recurring access to your capital.

- Are creating a diversified portfolio that includes alternative investments.

Many Groundfloor investors use note laddering as part of a broader strategy to balance liquidity needs with long-term wealth-building goals.

Important Note About Note Maturity Dates

When building a note ladder, it’s important to understand how Groundfloor Note timelines work.

Groundfloor Notes mature according to the schedule outlined in each offering, not a rolling period that begins on the day you invest. For example, if you purchase a 3-Month Note later in its offering window, the Note may mature sooner than three full months from your investment date. You’ll receive your principal and any accrued interest when the Note matures, but your investment may not have been outstanding for the entire three-month offering period.

The same concept applies to the 1-Month and 12-Month Notes. Every Note has its own offering period, issue date, and maturity date. Before investing, review the Note details so you understand exactly when your capital is expected to be returned and how that timeline fits into your laddering strategy.

Many investors intentionally combine Notes with different maturity dates to create recurring access to capital throughout the year. Understanding those schedules is one of the keys to building an effective note ladder.

Frequently Asked Questions

Notes are fixed-income investments offered by Groundfloor that provide a stated rate of return over a defined term. Investors can choose from multiple term lengths, including 1-Month, 3-Month, and 12-Month Notes, depending on their income and liquidity goals.

Groundfloor Notes are backed by diversified pools of real estate loans originated through the Groundfloor platform. This structure is designed to provide investors with exposure to private credit and real estate-backed investments without having to select individual loans themselves.

Unlike savings accounts, which have variable rates that can change at any time, Notes offer fixed returns for the duration of the investment. When a Note reaches maturity, investors receive their original principal plus earned interest.

Since launching Notes in 2018, Groundfloor has paid 100% of principal and interest owed to Note investors on time. It is the most popular investment product on the Groundfloor platform.

Note stacking is another term for note laddering. Both describe the practice of building multiple Note positions that mature at different times.

While Groundfloor Notes have minimum investments starting at $100-$1,000, many investors find that note laddering becomes most effective with $10,000 or more to invest. This allows capital to be spread across multiple Notes and maturity dates, creating a more meaningful cash flow strategy with recurring access to principal and interest. Investors use Notes as alternatives to their traditional savings accounts and other fixed-income investing products like CDs.

Your principal plus interest is returned when each Note reaches its defined maturity date. By staggering maturity dates, investors can create rolling monthly, quarterly, and yearly access to capital and interest payments depending on the structure of their ladder.

Yes. Many investors choose to reinvest matured capital plus interest into new Notes to maintain their ladder and continue generating income.

The answer depends on your goals. Savings accounts may prioritize liquidity (although many have withdrawal limits), while note laddering is designed to generate higher fixed returns while creating recurring opportunities to access capital through staggered maturities.

Build Your Own Note Ladder

Ready to build your own note stacking strategy?

Invest in Notes today to build your own ladder, or schedule a call with the Groundfloor team to build an approach that fits into your portfolio.

Illustrative examples assume rates remain constant and all matured Notes are immediately reinvested at the same rate. Actual returns will vary based on investment timing, offering dates, and future Note rates. The comparison uses the national average 12-month CD rate of 1.65% APY, as reported by the FDIC, as of July 2026.